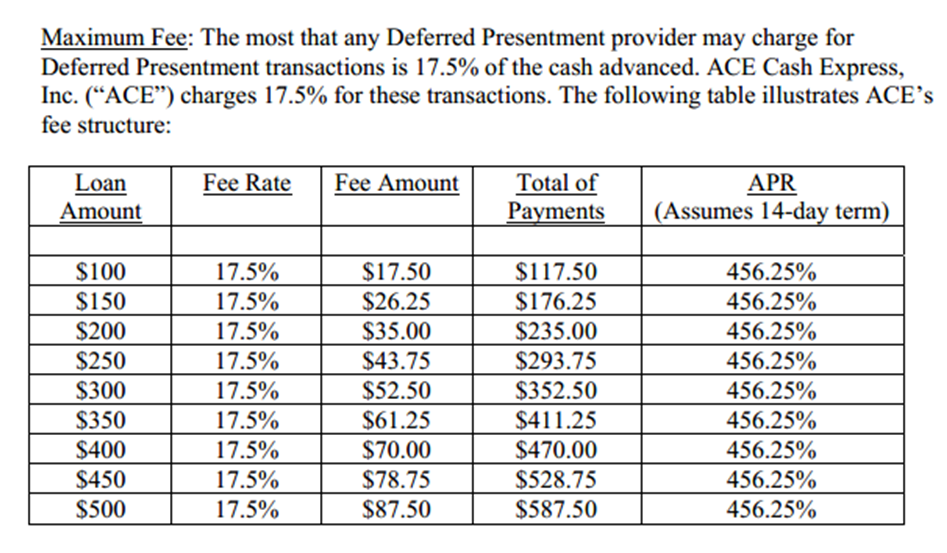

Lenders understand it given that a serious cause of what you can do to pay finance Leave a comment

Financial institutions play with numerous symptoms to gauge your ability to invest right back obligations. Perhaps one of the most crucial is your debt-to-money (DTI) ratio.

What is actually Your debt-to-Income Proportion?

/arc-anglerfish-arc2-prod-mco.s3.amazonaws.com/public/UMYZWYGCQNDP3JW6MAH3XZN73E.jpg)

The DTI ratio represents the latest ratio of the costs relative to the revenues. Although called a proportion, this is often shown as a portion. It strategies exactly how much of your income visits paying debt. The higher your DTI http://paydayloancolorado.net/minturn/ ratio, the fresh faster area you may have left to cover alot more bills versus a hitch. Using up so many expenses too quickly commonly place your profit to your jeopardy.

You should not mistake your DTI ratio for the cashflow, which is the amount of money are relocating and you may off your earnings. The costs that are part of your DTI should be recurring and ongoing. These all possess an important lowest amount you need to shell out monthly. Thus, never assume all the expenses are included in the DTI. Casual expenditures and you can tools by way of example, come out associated with umbrella. Because they are susceptible to next write-offs, fees are also not mentioned.

Loan providers have a tendency to look at your DTI proportion to determine if or not you is borrow cash at all. And with good reason, also. If the DTI proportion is too highest, you do not have enough action place when it comes down to a great deal more personal debt. Research has shown that folks with higher DTI rates be much more almost certainly to default to their mortgage loans.

Pigly’s Tip!

Avoid being aching for people who nonetheless don’t become approved. You can always alter your DTI ratio by paying from your debts basic.

Because the beneficial as your DTI is really as an assess, it has got its restrictions. First and foremost, their image was unfinished. It will not make use of the taxes, for example. Because and additionally targets minimum payments, it wouldn’t be a precise reflection regarding how much cash you may spend repaying costs. Additionally, whilst excludes your day-to-day expenditures, it will not directly portray the genuine funds.

Fantastically dull Financial Courses

Lately, what’s needed must make an application for mortgage loans had been less strict. Anyone could borrow money to have home without the need to establish one to they might pay it off. It, of course, turned into a dish to possess crisis. Less conscientious lenders invited visitors to borrow more funds than simply it can afford. New ensuing casing crash are a contributing factor to the Late 2000s Overall economy.

The relationship ranging from reckless credit and houses crash failed to wade undetected. In the aftermath of your own Great Market meltdown, statutes including the anti-predatory credit operate were applied. Lenders was indeed no more allowed to signal mortgage loans as opposed to verifying the newest borrower’s ability to pay-off. And also this caused it to be more challenging for all of us to help you meet the requirements also getting subprime mortgage loans.

Creditor Believe

Your own DTI proportion is one of of numerous steps accustomed learn the exposure because the a debtor. Loan providers believe in methods such as these to find out if or not you might be able to shell out. Institutional loan providers like less risky borrowers. Talking about people who find themselves planning to build uniform normal money across the longterm. It isn’t adequate that borrower matches a certain money top. However they need show they can pay during the a beneficial consistent styles.

Bank count on try pivotal in order to protecting an educated loan you can manage. Certain loan providers cannot extend hardly any money after all for many who look too risky. Some days, they won’t offer the higher number you desire. This will rapidly put a good damper into plans to purchase property. Thus, winning the newest count on of your bank is the vital thing so you can saving money when credit.